Matt Dalgleigh from Episode 3 presenting his forecast for cattle prices in 2025 and 2026 at last week’s WagyuEdge conference in Perth.

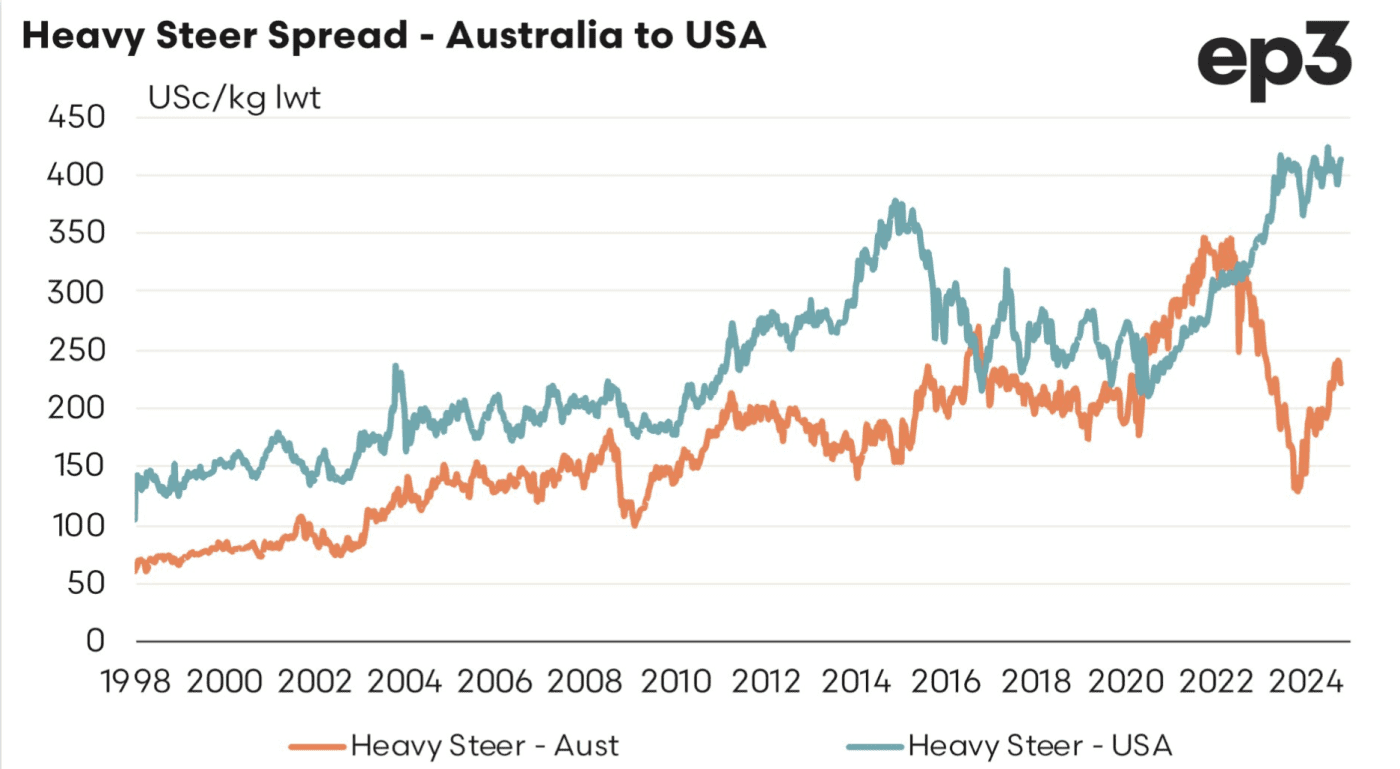

PRICES for Australian heavy steers are set to rise from an average of 365c/kg liveweight in 2025 to 400c/kg in 2026, according to an outlook presented to the 2025 WagyuEdge conference by economist and market analyst Matt Dalgleish from Episode 3.

In terms of pricing for Wagyu F1 feeders, Mr Dalgleigh’s modelling points to a 470c/kg liveweight average this year rising to an 850c/kg average in 2026 as premiums recover.

His forecast is based on expectations of normal rainfall, a moderate view on the Australian dollar tracking around US63c next year, and supply and demand levels trending in line with MLA and USDA estimates.

His forecast is based on expectations of normal rainfall, a moderate view on the Australian dollar tracking around US63c next year, and supply and demand levels trending in line with MLA and USDA estimates.

The primary threat to the forecast he sees is the potential for a slowdown in the Chinese economy or a return to drier than average seasonal conditions in Australia, which would adjust down the forecast for F1 feeders to the low-to-mid 700c range depending on severity of either, or both, outcomes.

The positive price forecast is based on a range of factors including:

Australia is moving back to a rebuild phase following the recent northern rainfall

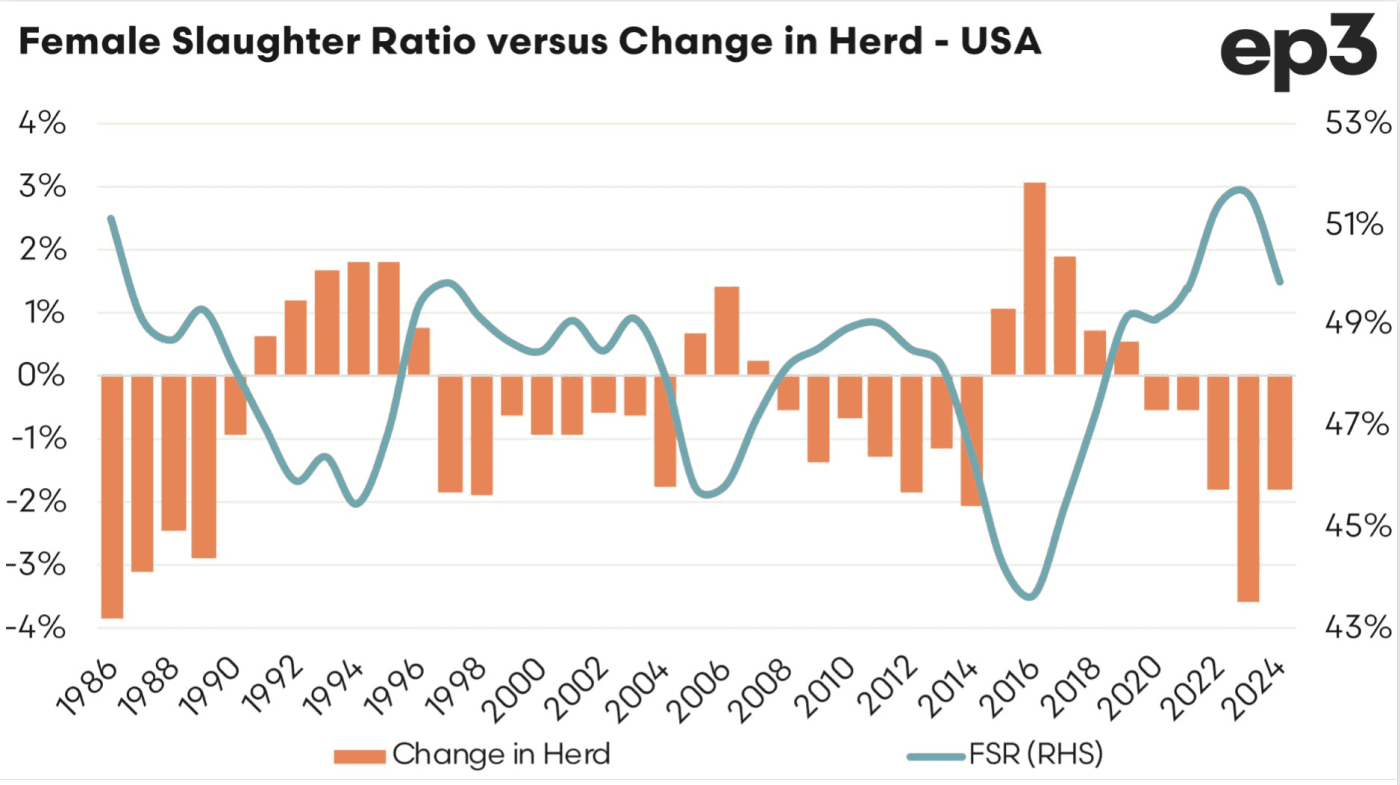

The Female Slaughter Ratio (FSR), which indicates whether the Australian herd is in a liquidation or rebuild cycle, is trending down back toward a rebuild phase, with recent rainfall in the north likely to exacerbate that trend in coming months, Mr Dalgelish predicts.

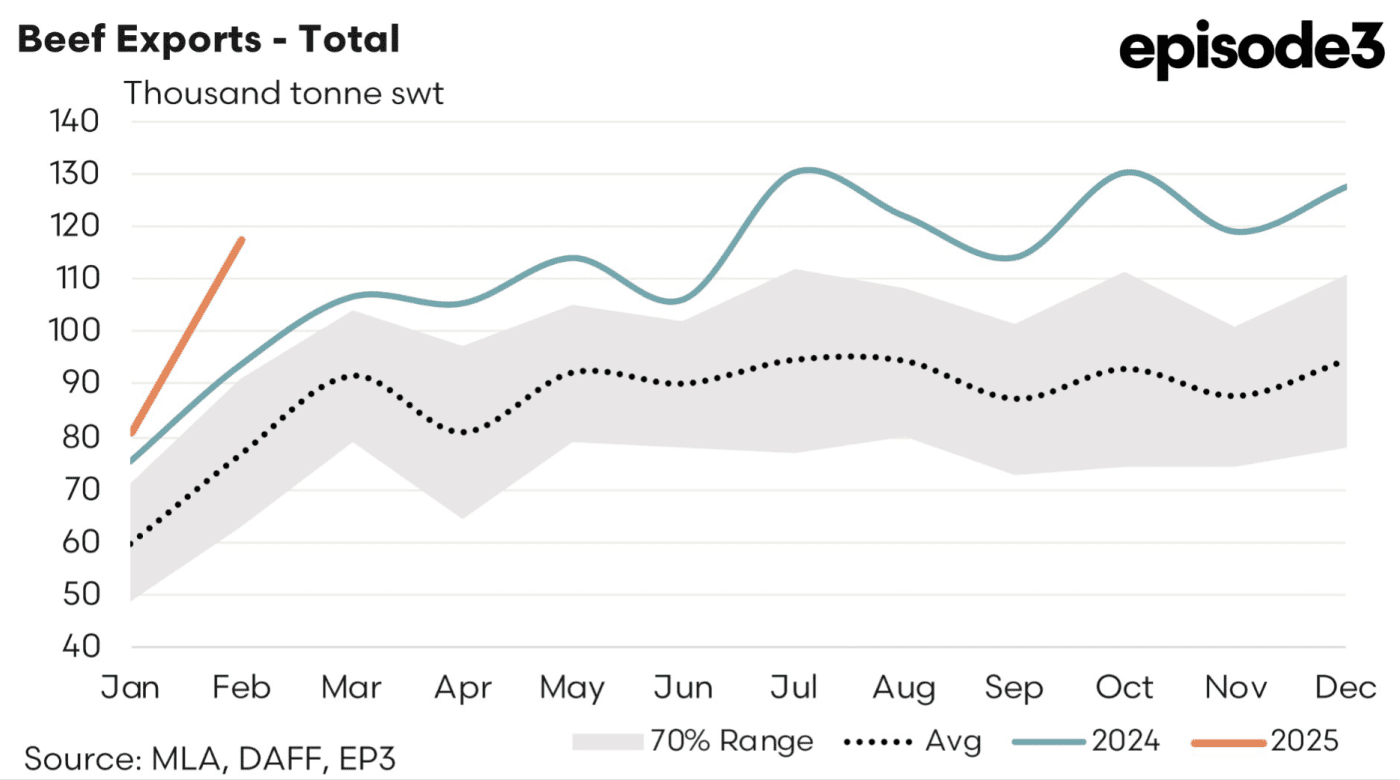

Tight global supply

Globally we are in a period of tight supply across several beef producing countries. This has contributed to record flows of beef exports leaving Australia, with new volume records set in January and February.

“The broad supply and demand picture is a very positive one,” Mr Dalgleish noted, with US demand for Australian beef increasing, China re-engaging with Australia and demand also growing elsewhere in the world in markets such as the Middle East/North Asia and South East Asia.

The US is trending towards a herd rebuild, which will put further upward pressure on prices

The US is in its sixth year of liquidation, but at the end of February, the US Female Slaughter Ratio was at 49.3pc and trending towards 48pc, the point where the US herd cycle typically flips from liquidation into rebuild phase.

Mr Dalgleish said more will be revealed when data for April is released, but there is an expectation the US FSR is on the threshold of entering a rebuild phase, with tightening supplies leading to the rising price signals being seen in the US:

Trump tariffs

The 10 percent tariff on Australian beef into the US would keep Australian beef competitive and would also help to Australia to maintain competitive access in other markets as well.

“The dynamic as it stands now, because it does change sometimes daily, but the dynamic is broadly positive even with the tariff there of 10 percent.”

Mr Dalgleish also highlighted a number of structural changes currently playing out in the Australian cattle industry:

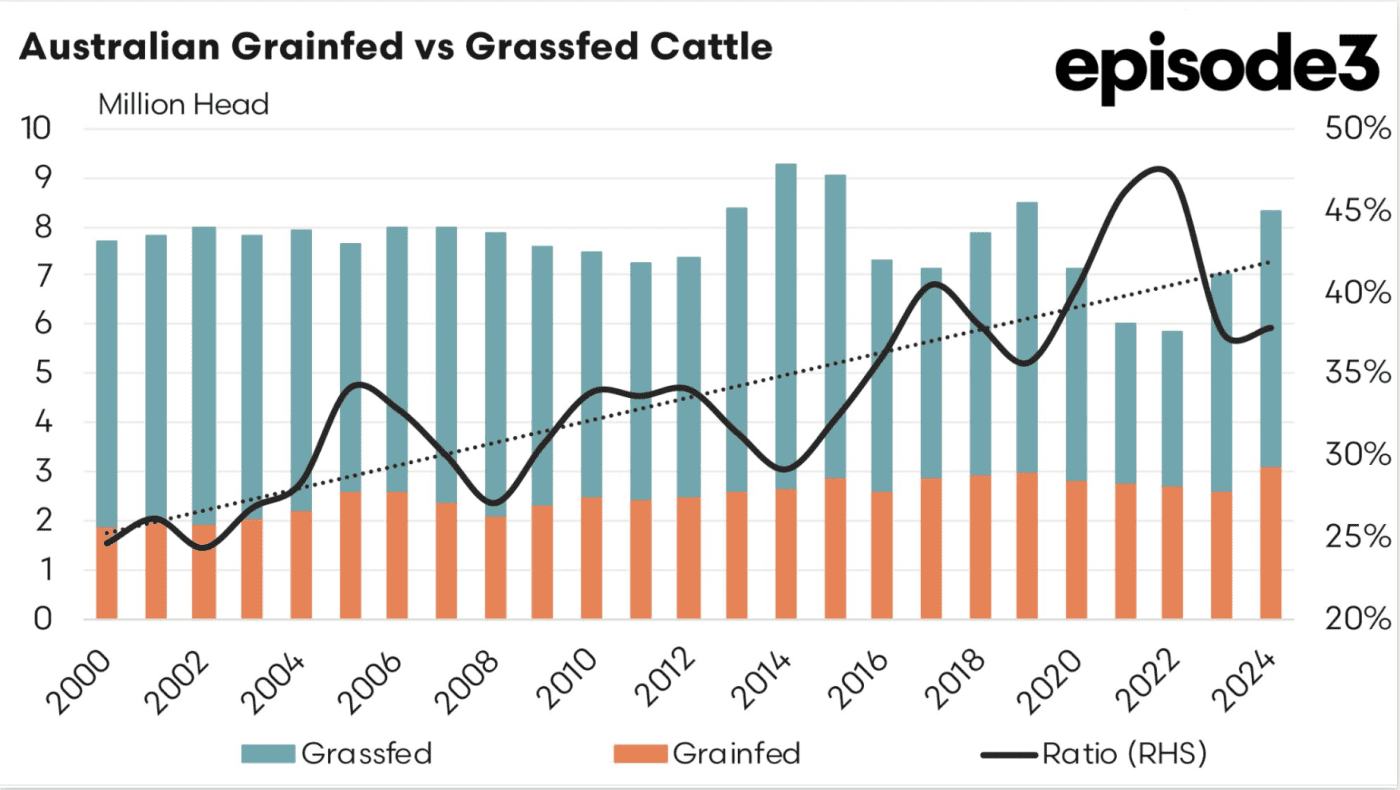

Grainfed production as a percentage of turnoff is growing, likely to hit 1.6 million head this year

In the early 2000s about 20 percent of cattle turnoff in Australia was grainfed. Now the ratio between grassfed and grainfed is nearing 40pc (as shown by black line in above chart).

In the early 2000s about 20 percent of cattle turnoff in Australia was grainfed. Now the ratio between grassfed and grainfed is nearing 40pc (as shown by black line in above chart).

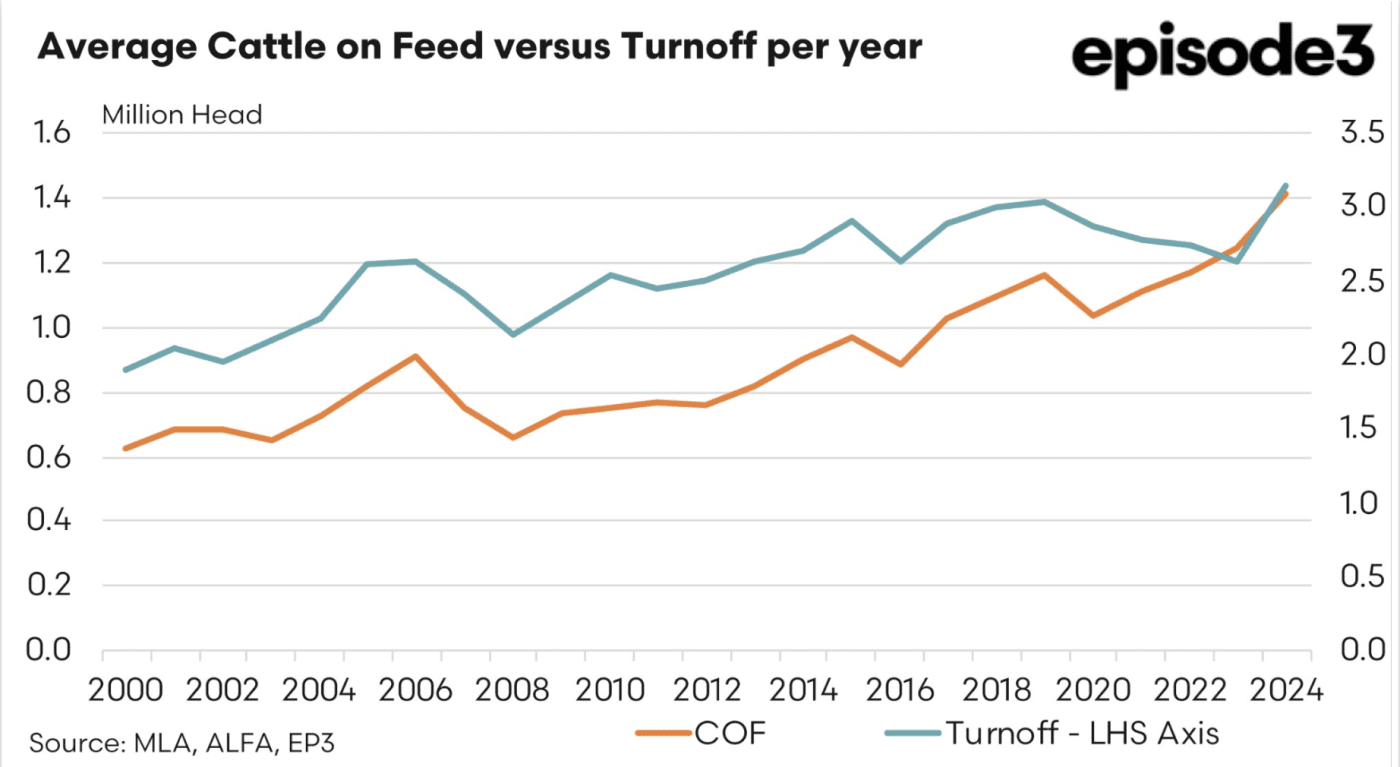

Australian cattle on feed numbers have increased from 600,000 head 25 years ago to 1.4 million at the end of 2024.

Australian cattle on feed numbers have increased from 600,000 head 25 years ago to 1.4 million at the end of 2024.

“I think we are going to be touching towards 1.6 million cattle on feed this year.

“I think there is another 150,000 head of extra capacity coming online this year as well, so that sector is going to continue to grow in the next decade.

“Despite the fluctuations and those peaks and troughs I think we are heading toward a 50-50 ratio by the end of this decade and into the 2030s.”

Cattle being held on feed for longer

Cattle on feed over the last 25 years in Australia have increased by about 127 percent.

Cattle on feed over the last 25 years in Australia have increased by about 127 percent.

And yet the turnoff has only gone up about 65pc.

Between 2000 and 2014 feedlots were averaging around three turnoffs per year, but in 2018 that number dropped to about 2.6, and then 2.1 in 2023.

The data is reflecting the trend toward cattle being held for longer, as more Wagyu and long-fed Angus cattle have entered feedlots.

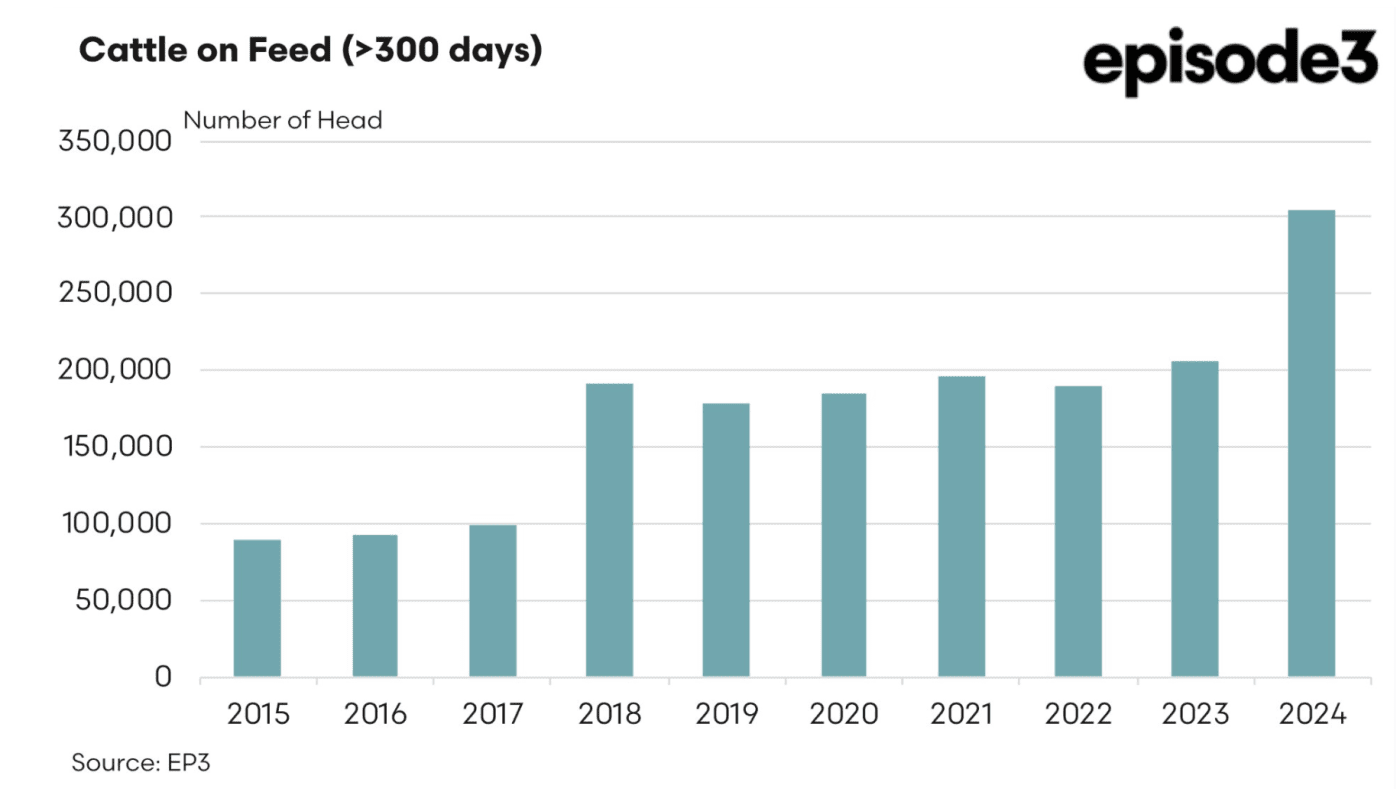

“Since 2015 cattle on feed for more than 300 days have almost tripled, with the number of Wagyu cattle on feed now over 300,000 head.

That has corresponded with big growth in Wagyu registrations since 2016. Similarly, MLA producer survey results demonstrate that Wagyu has climbed from seventh to fifth most used breed.

That has corresponded with big growth in Wagyu registrations since 2016. Similarly, MLA producer survey results demonstrate that Wagyu has climbed from seventh to fifth most used breed.

Mr Dalgleish noted there has been a slight drop in numbers since the end of 2024, with MLA statistics recording a 0.1 percent decrease in Wagyu as a percentage of the national herd from 2002 to 2024.

“So that little drop there is a sign of the market just taking off a little bit of steam, but still we’re sitting at three times the amount of Wagyu on feed when you look at the trend over the last decade,” Mr Dalgleish said.

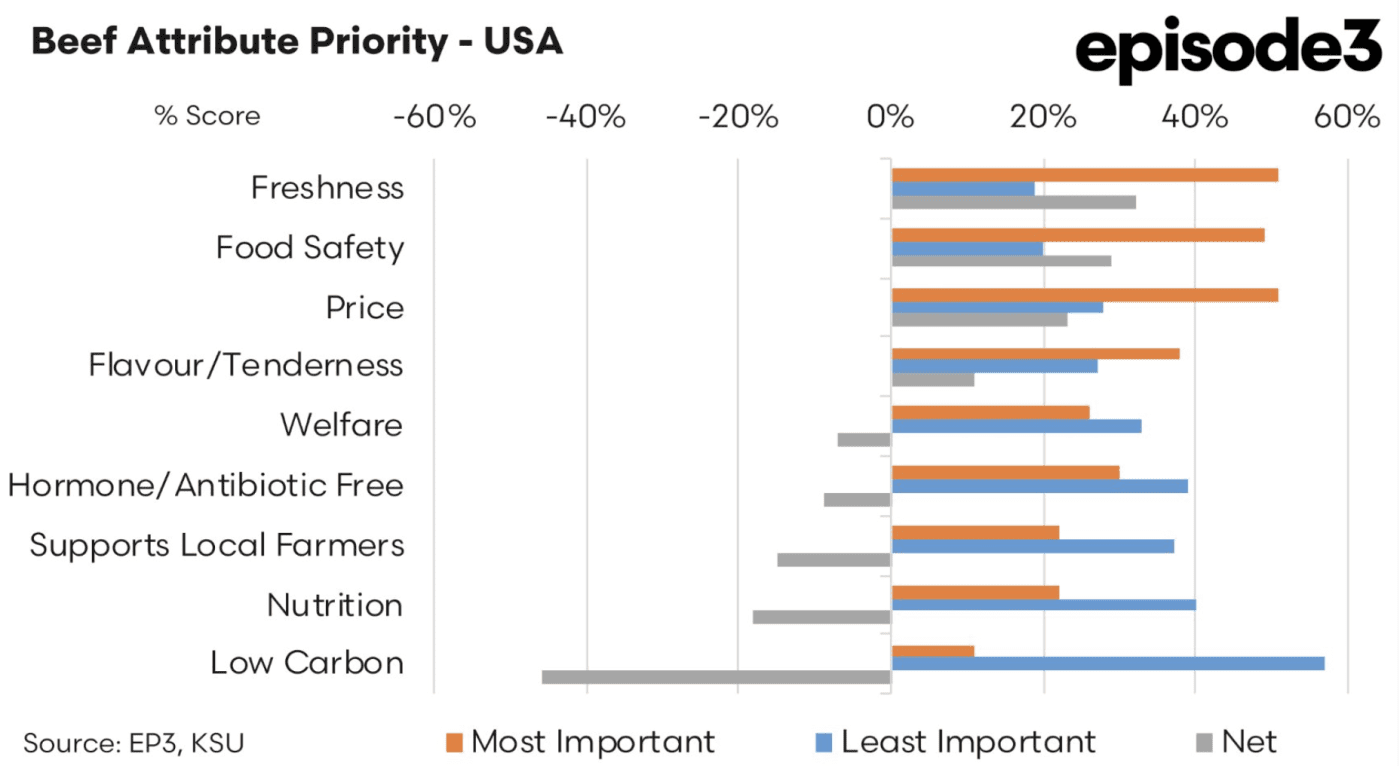

Consumer signals align well with Aussie beef

This chart highlights what the attributes US consumers rate most highly when shopping for beef, with flavour, tenderness, price, food safety, traceability for freshness all rating highly.

“So we are an incredibly competitive product in terms of the key attributes they are looking for.”

HAVE YOUR SAY