RECORD Australian cattle production and beef exports are expected in 2025 as carcase weights remain high.

Australia’s cattle herd is expected to decline slightly as record production, slaughter and exports meet demand, according to Meat & Livestock Australia’s 2025 Cattle and Sheep Industry Projections report released this morning.

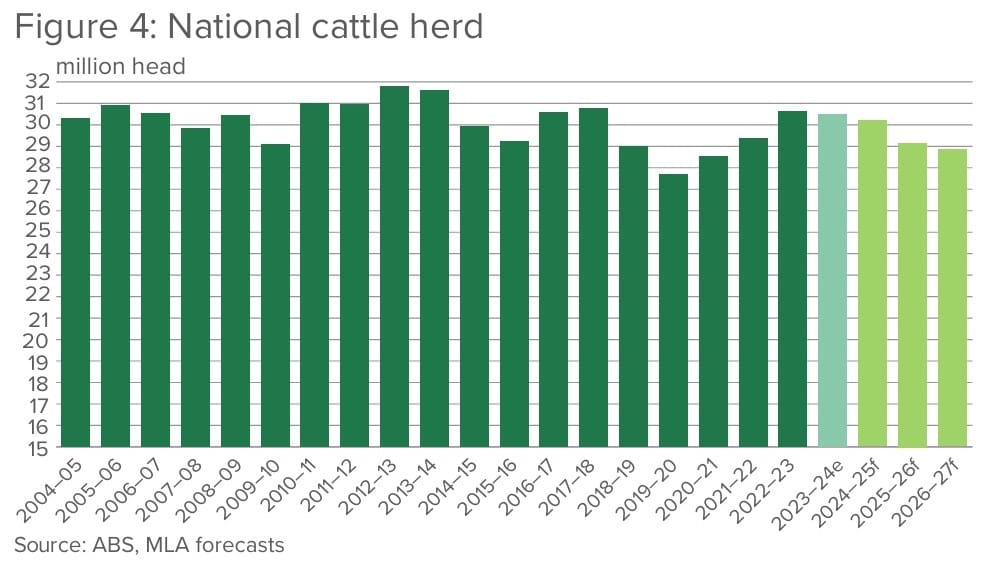

The cattle herd is projected to fall by 1.4 percent to 30.1 million head in 2025, due to increased turn-off of older breeding cows and dry conditions in Southern Australia. Next year will fall to 29.2m head, MLA forecasts.

These numbers show some closer alignment with ABARES own herd forecasts, than has been seen in recent years. ABARES has this year’s herd at 29m, 28.8 next year and 29.42m in 2027.

Varied climatic conditions across Australia have contributed to herd stability over the past 18 months. MLA projections indicate that southern states will continue to turn-off large numbers of cattle due to tough seasonal conditions in large production areas, driving a decline in the national herd through to June 2025.

A 47 percent female slaughter ratio is the industry benchmark for determining whether the national herd is in a restocking, stable or destocking phase. In December 2024, the FSR was 51.8pc – marking the third consecutive quarter above the benchmark – confirming a sustained destock.

MLA’s herd estimates are adjusted based on the FSR, alongside additional factors including the age of cows at turn-off and whether turn-off is driven by drought or herd cycle dynamics.

Conversely, northern Australia has experienced a strong, if somewhat late wet season in 2024, strengthening the northern herd and supporting production..

However, models suggest conditions in the north could shift over the forecast period, supporting projections that turn-off will remain high, resulting in three years of herd reduction.

A productive herd, combined with significant increases in carcase weights, has resulted in record beef production, despite fewer cattle, the report said.

Producer concern remains focused on production costs, the Projections report concludes. Businesses that have invested in efficiency measures have experienced some relief, however rising input costs –such as labour, fuel, transport and utilities – continues to constrain profitability.

Emerging concerns regarding compliance costs, rates and market volatility may also contribute to future uncertainty within the sector.

Slaughter

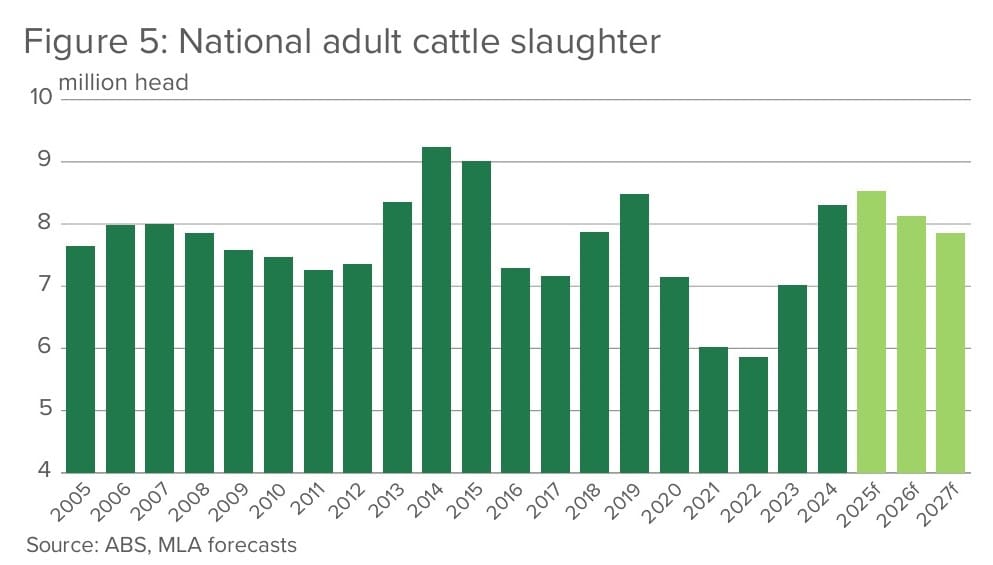

Slaughter cattle supply is expected to remain solid through 2025. With the herd’s increased turn-off capability and a slight rise in stock turn-off rates, slaughter is projected to increase 2.8pc this year to to 8.54 million head. However, as the herd shrinks, turn-off capability will be impacted, leading to an estimated 4.7pc reduction in slaughter to 8.13m head in 2026, followed by a further 3.5pc decrease to 7.85m in 2027.

Carcase weights are forecast to increase by 2.4kg in 2026, back to 309.8kg/head with another 8.4kg rise in 2027 to 318.2kg. Beyond seasonal variations, long-term increases in carcase weights are expected as the industry continues investing in genetics, the feedlot sector, and growth in Bos taurus breeds.

According to MLA managing director Michael Crowley, the Cattle and Sheep Industry Projections show that the red meat industry is ready to respond to global demand in 2025.

“Record production and elevated slaughter rates are being met with strong demand from well-established relationships with customers throughout the global supply chain,” Mr Crowley said.

The Cattle and Sheep Industry Projections are an important tool for the industry to understand the forecast conditions facing the industry.

“By consulting with producers, processors, agents, and government, MLA creates a clear forecast of the national herd and flock, slaughter, production and carcase weights for the cattle and sheep industries,” Mr Crowley said.

Australia produced more beef than ever in 2024, despite slaughter volumes being 7pc below the previous record in 2014. This was due to higher carcase weights, primarily due to increased grainfed production.

“Producers are growing more efficient and productive cattle compared to 10 years ago. This is important considering the significant global demand for beef will continue this year, leading to another record production year,” Mr Crowley said.

“Australia is currently in an opposite supply cycle to major beef-producing competitors such as the United States and Brazil. As the US begins its long-overdue herd rebuild and drought conditions in Brazil ease, global beef supply is expected to tighten.

As record production continues into 2025, efficient logistics and supply chain management will become increasingly important.

“Australia is well-positioned to achieve record production and export volumes once again,” Mr Crowley said.

“With increasing carcase weights, storage space has become more valuable, and efficient logistics are now essential to maintaining processing flow and preventing bottlenecks in the supply chain.

“Looking ahead, Australia’s investments in domestic production, processing capacity, and global trade relationships have positioned the cattle sector well for the next few years.”

Global demand for beef remains strong, the report notes.

A continued reduction in the US beef herd, with varying forecasts of a rebuild, will sustain US demand for Australian lean beef and preserve access to high value markets. Additionally, a projected decline in Brazilian slaughter may reduce competition in commodity-focused markets.

Australia is well-positioned to achieve record production and export volumes once again, however, limitations in processing capacity could hinder domestic processors’ ability to meet demand, the report warned.

Processors have resolved many labour and throughput limitations, but cold storage and logistics constraints have emerged due to higher production per animal.

Despite potential capacity limitations, processors have historically adapted to volatile supply conditions. Strong global demand aligns with a projected period of high turn-off, placing the Australian cattle industry in a cautiously optimistic position.

Labour constraints

Labour constraints have changed Labour access remains a key challenge, exacerbated by the disruptions caused by COVID in 2019-20.

Labour shortages were a limiting factor in 2019, preventing the industry from achieving record processing volumes during the drought. Since then, processors have heavily invested in workforce retention.

Processors have relied on PALM labour, and have invested in accommodation and pastoral care to support it as a sustainable workforce. While this has provided greater stability, it has also introduced a fixed labour cost, making it harder for processors to adjust workforce levels in response to supply fluctuations.

- Click here to access Sheep Central’s report on MLA’s 2025 Sheep Industry Projections

HAVE YOUR SAY