TWO big ‘known unknowns’ are driving the eastern Australian slaughter markets this week.

The first is the massive monsoonal trough weather system that’s threatening to dump 100-150mm and more across large parts of Queensland, NSW and the Northern Territory over the next week.

The first is the massive monsoonal trough weather system that’s threatening to dump 100-150mm and more across large parts of Queensland, NSW and the Northern Territory over the next week.

The second is more sinister – the threat of punitive tariffs on beef exports to the US, starting Thursday next week (Australian time).

At this stage, it’s impossible to tell which will be more impactful, but for once at least, the weather may be the more predictable of the two.

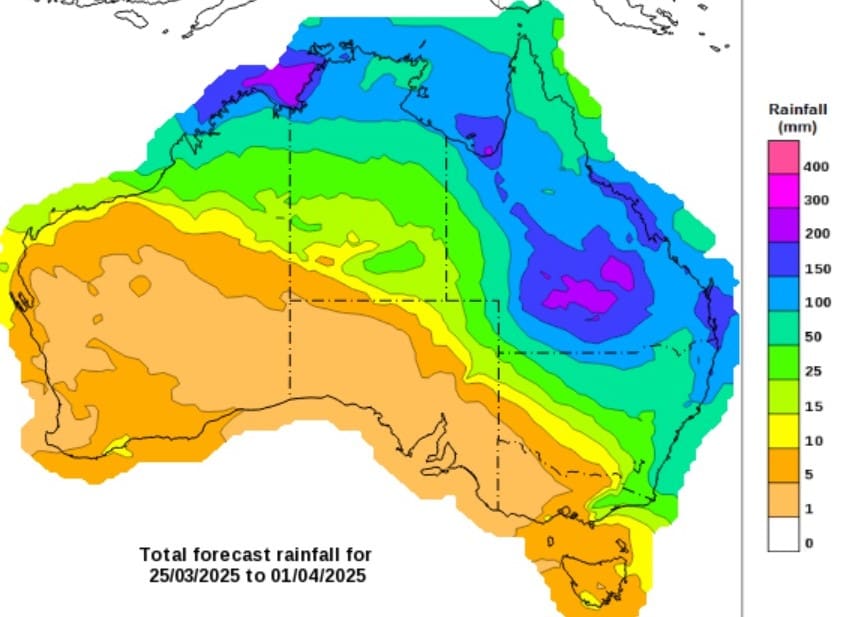

As the BOM eight-day forecast published below shows, there’s heavy rain forecast of 100mm or more (light blue) across a wide belt of Queensland, tipping into northern NSW, and across the top end and Kimberley region, through to 1 April. More intense areas in Central Queensland could receive +150-200mm.

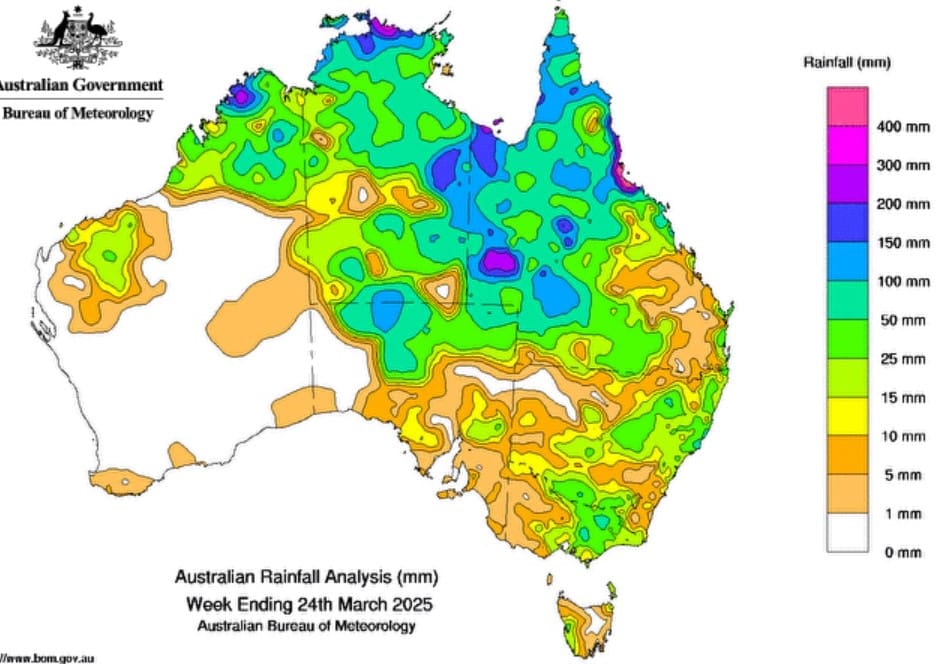

That comes on top of some big falls already received over the past seven days (see second BOM map below) widely dispersed across the Northern Territory, the western and northern half of Queensland, and into South Australia’s pastoral zone.

One regular Beef Central reader remarked this morning that he could not remember a more widespread significant rain weather system across the continent in recent times.

If the rain delivers as predicted, it will have profound impacts on the cattle supply/demand dynamic in a number of ways.

The first, of course, is significant late season grass and herbage growth, heading into winter, assuming conditions stay reasonably warm until after Easter. That will be particularly welcome in those areas of northern Australia that were rapidly drying off since early February.

The second is the likelihood of substantially reduced slaughter cattle supply pressure. Only a week ago, many beef plants in Queensland and northern NSW were heavily booked for spaces deep into April, either priced, or unpriced (kill slots only).

That supply pressure is likely to evaporate if the rain event is anything like that portrayed on BOM’s forecast.

Reduced competition for kill space could in turn lift competition from processors in coming weeks, with substantial margins still evident on both slaughter cows and grass steers due to international demand for Australian beef, led by the US.

In the more immediate sense, processors have already fielded delivery cancellations early this week from rain that’s already fallen, but the impact to this point on operations has been moderate. Some plants are still working through surplus cattle left over from the Cyclone event three weeks ago, held over for a variety of reasons.

Next week may prove to be a different story however, with prospects of reduced kills in Queensland.

While some of the biggest rain that’s fallen so far has been in Queensland’s far western Channel Country, its still too hot and too early in the season for major slaughter cattle shipments from that region. Longer-term, though, its likely there will be plenty of beneficial flooding on the Channel Country systems across the Diamantina, Georgina and Cooper Creek.

Nevertheless, major western Queensland arterial transport routes like the Landsborough Highway were shut in recent days, and some regional cattle sales cancelled, including Charters Towers and Sarina.

Export beef processors in Queensland are clearly ‘banking’ saleyard-sourced cattle early this week, anticipating that supply challenges may emerge in the days ahead if roads are cut and paddocks inundated.

Tariff uncertainty

As reported yesterday, there’s been no clear signals that the uncertainty surround tariff imposts on Australian beef heading to the US before the next deadline of 2 April is yet affecting cattle markets. In fact, as described below, saleyards prices on export weight steers and cows have generally risen in the past few days.

Having said that, exporters report that US meat trading contacts ‘clearly had the jitters’ during discussions this morning, as the uncertainty around tariffs starts to close in. While prices in lean trimmings have held up well over the past week, volume of sales is currently well down, traders said (see yesterday’s report).

Over the hooks quotes

Direct consignment slaughter grids in Queensland are mostly steady this week.

Grid offers seen this morning have southern Queensland on 580c/kg on good quality heavy cows, and 640-650c/kg on four-tooth heavy grass ox.

Central Queensland plants are 20c/kg behind that, suggesting a little more supply pressure (up to today, at least), and Townsville, now 50c/kg behind southern Qld, with cows 530c/kg and steers 600c. That follows some 10c drops in Central Queensland last week.

“We’re back!” – southern processors reappear in QLD

In southern states, processors are clearly running out of killable cattle. Grids compared with Queensland are now 30-40c/kg apart.

In southern NSW this morning, one grid had grass steers four teeth 690c, and cows 610c. Processors in eastern parts of South Australia were this morning offering 680c on the bullock and 630c/kg on cows. Those numbers are up another 10-20c on last week.

Some big margins are now starting to appear between Queensland rates and southern states, prompting southern processors last week to start purchasing numbers out of Queensland – despite the hefty 25-30c freight bill to get them home. The same thing happened last year, when southern processors were a constant presence in the Queensland market for most of the year.

Reports suggest one large Victorian processor is currently offering 610c/kg dressed weight on good Queensland paddock cows, delivered Morven.

Why dressed weight at the plant, instead of live over the scales Morven? The answer is that southern buyers were getting a hiding in yields buying Queensland cattle on a liveweight basis last year. Yields after a 1700km transit are much worse than a typical 350-500km transit in southern Queensland. It won’t take long for Queensland vendors to figure that out.

Another source (unsubstantiated) suggested another southern processor was yesterday offering 305c/kg liveweight for +600kg cows delivered Dalby. That would price the cow (51.5pc dressing) at 592c/kg dw at Dalby, but more like 630-640c/kg delivered Victoria.

There were a handful of cattle picked up by Victoria’s Australian Meat Group out of Dalby sale for the first time last Wednesday, and Ralph’s out of Seymour, VIC was purchasing a few at Roma sale this morning. Expect to see more of that activity in coming weeks.

Saleyards prices lift, but numbers down

Rain has impacted numbers offered at some physical sales early this week, but prices on slaughter types were generally stronger.

Gunnedah yarded 1835 this morning, about half lasty week’s yarding. Cows dominated the export cattle supply. There was a good supply of well finished cattle to suit processors. Strong demand from processors resulted in the well finished grown heifers selling to a considerably dearer trend. That demand carried into the cow market where all classes were dearer, with well finished heavyweights selling as much as 25c/kg dearer.

Wagga sale yesterday saw a slight rise in numbers to 6445 head, due to a lack of significant rainfall across the region. On the export front, the market was lively as all buyers vied for a share, resulting in notable price spikes of 25-30c/kg. Heavy steers and bullocks made from 344-406c. Heavy cows also saw a gain of 10c, with prices from 276-310c. The middle run of leaner types sold at a range of 250-272c.

Wodonga numbers this morning were unchanged at 1200 head, almost half of which were cows. There was a bigger field of export buyers present. Export cattle were the highlight, with competition lifting over all categories. Heavy steers averaged 365c. Bullocks sold to a larger group of buyers and bidding duels at times were lengthy. Prices improved 22c to average 392c/kg. A large offering of cows met a bigger field of buyers. Heavy cows traded from 282-328c/kg improving 15c, while the leaner heavy cows gained 9-16c. D2 and D3 cows under 520kg made from 248-276c/kg.

Numbers at Roma store sale this morning crashed due to rain, yarding 3600, about half of last week. A preliminary report (full details tomorrow), saw steers 400-480kg sold to improved rates and made to 368c/kg, while grown steers +600kg sold to 361c almost 30c/kg dearer than the last sale.

- There’s been an extraordinary reader response to Beef Central’s Top 25 Livestock Transporters feature launched yesterday. The feature will unfold over the next three weeks in reverse countdown fashion. Click here to access.

Known – Today 25.3.2025 Trump just announced 25% tariff on any Country buying ANY oil from Venezuela this for the stupid means;

China, who in 2023 bought 68% of the oil exported by Venezuela will be in a April 2025 US China Trade War

Regardless of the Australian price or percentage of the “unknown” imaginary tariff the USA might or might not impose the US needs more Australian Cows for its Burgers – because they dont have enough beef and its expensive there and its cheaper here in Australia so cheap its actually disgusting to watch… and Aussie Producers are being constantly fed the stuff that comes out of the wrong end of the cow by the Rural Media and Processors.

The US is the world’s largest beef producer (at very low pre 1957 cattle numbers), the worlds second-largest importer, and the second-largest exporter by volume.

The US ironically is playing mind games with Australian Farmers its switching its premium beef cuts sold for premium prices to its foreign consumers in Asia China Japan Korea and Hong Kong and importing cheap (not for long) Australian Beef at absolute bargain discounted prices 0.63c Australia dollars at less than two thirds of their money bought in kilograms twice the weight it then sells this Beef for US Dollars in pounds (under half weight in pounds)

The ultimate loser is the Australian Beef Producer who buys Dodge and Ford Utes Kenworth Mack Truck John Deere Tractors CAT Bulldozers… at 1.58 AUD but at really over double the cost in steers (x2.24) of what the US farmers pay…

N.B. A US steer is grain fed because of necessity not because of taste preference the USA winters are that harsh their cattle would die in snow if grass was their only diet… this alone makes Australian beef very competitive even after lot feeding.

(Even worse than the US beef export switch selling yearling Bos Indicus (Yak) live heifers to the Philippines Indonesia etc OMG talk about selling out the Aussie Farmer… and the poor Aussie heifer )

Question. How many 600 pound USA steers does it cost to buy a new Ford 2025 F 150 etc in the USA ?

( Answer is 25 )

$3.39 USA dollars per pound

x 2.2 to convert to Kilograms

= $7.35 per kilogram USD

= $11.64 AUD per kilogram liveweight

A 600 pound US Steer sells for $2034 USD ($3222 AUD)

An equivalent 272 Kilogram Australian Steer sells for $952 AUD ($601 USD)

How many 272kg (600lb) Steers does it take to buy a Ford 2025 F 150 in Australia

( Answer is 112 )

I want my 62 Steers back Ford !

https://www.ams.usda.gov/mnreports/lswnfss.pdf

China will not buy any US Beef from next month April 2025.

The US is the world’s largest beef producer, but cant even supply its own Market its the second-largest importer, and the second-largest exporter by volume… only because it sells its premium grain fed beef and imports buys grass fed beef for its own market

Only *4 main Countries are really keeping it so cheap as Canada has similar beef prices…

Five countries account for 83 percent of U.S. beef imports in May 2024. These countries include Canada, *Australia, *New Zealand, *Mexico, and *Brazil.

The USDA forecast for 2025 beef exports is 2.5 billion pounds, or 11.3 percent **lower than the current 2024 forecast. ( converts to est 500,000 less 600 lb steers )

Now in 2024 Australia’s record export of Beef was 2.2 Million (not Billion) tonnes so how can the US supply its Markets… and how can Australia supply the Worlds increasing demand for Grass Fed (Organic) Beef let alone the USA’s 2025 lost market to China ?

Obviously the US exporting more Beef in 2025 is impossible when less Beef is produced.

Summing it up the economics rule number ONE

Less supply equals MORE demand BOOM.

Australian Beef will BOOM in 2025 and has absolutely zero to do with the weather rainfall report or USA tariffs on Australia’s Beef.

Processors and Exporters will be forced to pay record prices in 2025 to fill an insatiable demand for missing calories in a world that demands ever more steak and burgers.

N.B. Fish is far dearer than beef and is absolutely FREE to catch in the Pacific, Southern & Indian Ocean.